SP500 LDN TRADING UPDATE 21/1/26

SP500 LDN TRADING UPDATE 21/1/26

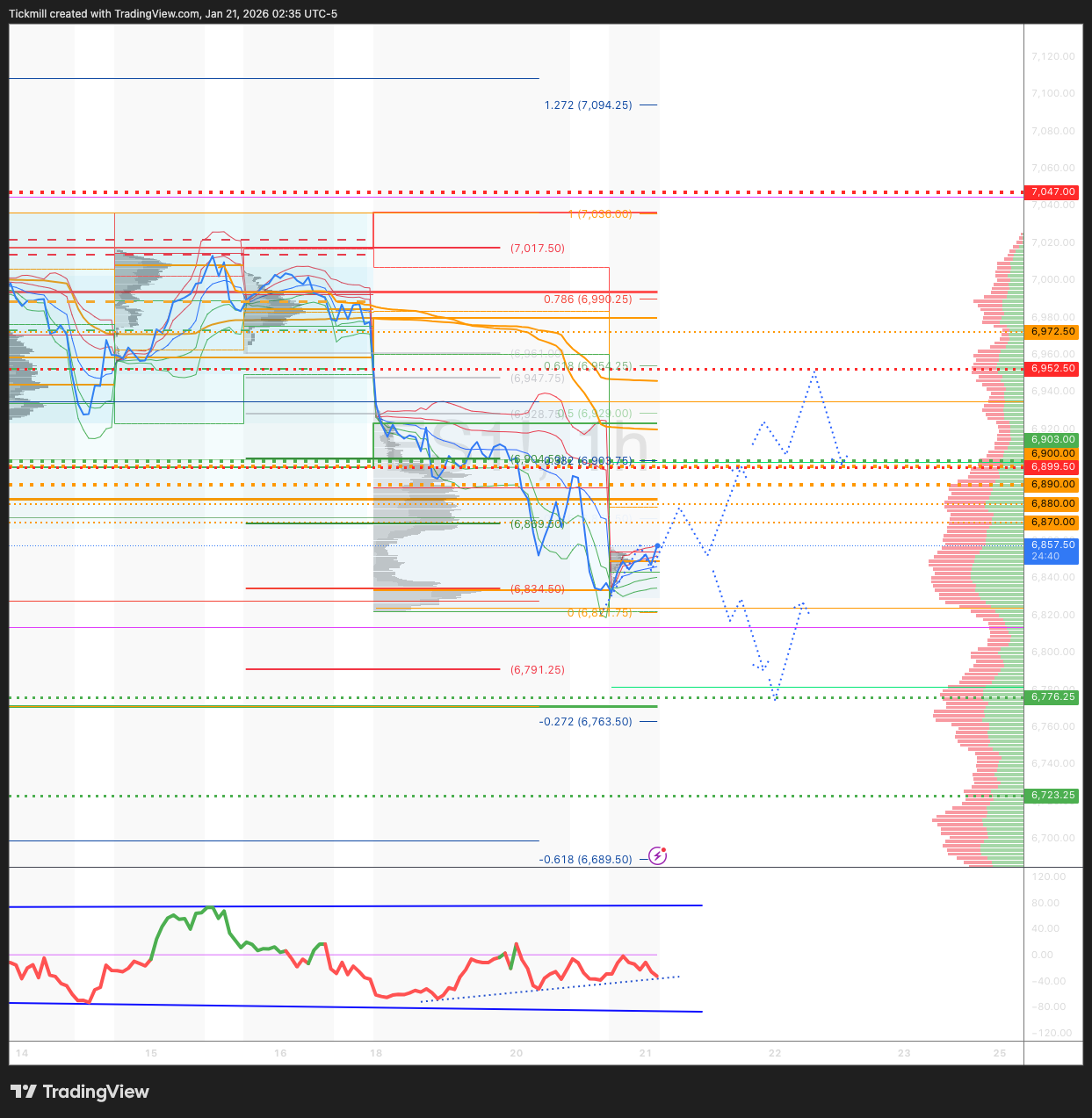

WEEKLY & DAILY LEVELS

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6900/6890

WEEKLY RANGE RES 7047 SUP 6903

FEB OPEX STRADDLE 6726/7154

MAR QOPEX STRADDLE 6466/7203

DEC 2026 OPEX STRADDLE 5889/7779

The area around the SPX aggregate gamma flip is at 6940. While the upside gamma is pronounced, it has somewhat smoothed since last week's vertical surface. The index has more leeway to rise. Based on the most recent analysis (Friday AH), the steep surface develops around 7030.

WEEKLY VWAP BULLISH 6969

MONTHLY VWAP BULLISH 6850

WEEKLY STRUCTURE – ONE TIME FRAMING DOWN - TBC

MONTHLY STRUCTURE – ONE TIME FRAMING HIGHER - 6775

DAILY VWAP BEARISH 6920

DAILY STRUCTURE – ONE TIME FRAMING DOWN - 69O4

DAILY BULL BEAR ZONE 6970/80

DAILY RANGE RES 6899 SUP 6776

2 SIGMA RES 6952 SUP 6723

VIX BULL BEAR ZONE 17.7

PUT/CALL RATIO 1.6

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY BEAR ZONE TARGET 6850>DAILY RANGE SUP

LONG ON REJECT/RECLAIM DAILY RANGE SUPPORT TARGET 6820

LONG ON ACCEPTANCE ABOVE WEEKLY BULL BEAR ZONE TARGET 6920 > 2 SIG RES

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - “RISK OFF”

S&P closed down -206bps at 6,797 with a MOC of $900M to sell. NDX dropped -212bps to 24,988, R2K fell -121bps to 2,645, and the Dow declined -176bps to 48,489. A total of 20.6B shares traded across all U.S. equity exchanges, surpassing the YTD daily average of 18.17B shares. VIX rose +663bps to 20.09, WTI Crude edged up +30bps to $59.53, the U.S. 10YR yield increased +7bps to 4.29%, gold climbed +192bps to 4,760, DXY fell -82bps to 98.58, and Bitcoin dropped -366bps to $89,543.

The "risk-off" sentiment was driven by two key factors: 1) a backup in rates and 2) Trump’s tariff threats, with the former playing a larger role. Japanese Government Bonds (JGBs) sold off overnight following PM Sanae Takaichi’s proposal to cut food taxes without clear funding plans. Meanwhile, President Trump proposed 10% tariffs starting February 1 on imports from eight European countries (Germany, France, UK, Netherlands, Denmark, Norway, Sweden, Finland), with a potential escalation to 25% by June 1 if no agreement is reached on his Greenland purchase proposal (implementation remains uncertain).

Bottom line (courtesy of Lee Coppersmith): This is a positioning-driven shock amplified by rising global yields rather than a structural macroeconomic issue. While tariff-related GDP damage is real, it is minimal, inflation effects are muted, and policy bias remains accommodative. The market is de-risking due to Japan no longer anchoring global duration. GIR notes that a 2-sigma move (~50bps today) over one month on the U.S. 10YR yield historically coincides with equity pullbacks. That level is ~4.6%, compared to late December lows.

Activity levels on our floor were rated a 6 on a scale of 1-10. The floor finished -369bps for sale versus a 30-day average of -95bps. Asset managers were net sellers at -$3B, while hedge funds remained balanced. Broad-based supply was observed across all sectors, with tech seeing the largest notional tickets from the LO community. Software supply continues to stand out, with residual sell orders from last week. Industrials remain net bought by both cohorts. Our prime team also reported heavy Info Tech selling last week, primarily driven by shorts, with software being the most net-sold subsector (net sold in 4 of the past 5 sessions). Aggregate net exposure and the long/short ratio in U.S. software stocks both ended the week at record lows.

Earnings post-bell: NFLX -5%, UAL +1% AH.

Macro-driven trading dominated today, with elevated ETF activity accounting for 37% of tape versus a historical average of ~28%. Russell 2000 marked its 12th consecutive day of outperformance versus the S&P 500, a streak not seen since 2008. Our macro desk continues to see strong demand for small caps. Top-of-book depth declined by over 60%, hitting its lowest level in two months. This is the final week of the estimated blackout window. Last week, we saw the first companies exit blackout, with Financials kicking off earnings. Typically, corporations exit blackout 1-2 days post-earnings.

Derivatives: The market saw ~2% selloffs in SPX and NDX, with skew steepening from last week raising the bar for volatility to perform during selloffs. Despite today’s selloff, skew bids were more pronounced than the move in volatility. Notably, IWM outperformed QQQ even as length was unwound. IWM has yet to underperform SPX this year, and the desk continues to favor RUT volatility over SPX or NDX volatility. Flows-wise, we observed sellers of volatility and theta as hedges were unwound. Attention now shifts to tomorrow’s VIX expiry and the hour leading into it, with Trump scheduled to speak in Davos. Tomorrow’s straddle is priced at 84bps (thanks to Gail Hafif).

IEEPA: No decision was made today. While the Court could theoretically add opinion days before February 20, nothing is currently on the calendar. This delay has implications for the EU tariff threat, as the prevailing view suggests that the longer the Court takes, the less likely it is to rule against the tariffs (thanks to Alec Phillips, GS Chief U.S. Political Economist).

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!